Tips to Improve Your Credit Score

We know paying off debt is a duty. Paying it early is sacred. While that is true for credit, the same may not be said for the credit FICO score. And though we have made them our holy grail for day-to-day finance, it is neither always accurate nor logical to apply credit scores as a standalone tool.

The psychology behind credit scores is still to promote good financial habits and to root out negative trends. But the blindsided notions and myths around credit scores must be checked. If you manage your own finances, these tips to improve your credit score will come naturally to you. And once that’s the case, you don’t need to worry as you will be on the right track to credit-worthiness.

Find our offbeat take on:

What’s a good credit score?

- How long does it take to improve a credit score?

- How to check your credit score?

What affects your credit score?

- Potential lenders and your credit

- The relation between credit history and credit score

What does & doesn’t improve your credit score?

- Things that have little to no impact on credit scores

- What makes your credit scores go up

… and answers to a range of other frequently asked questions.

What is a “Good” Credit Score

There is no one universal number to quantify the credibility of potential finance applicants. Different Credit Rating Agencies (CRA) evaluate credit risks through complex formulas involving multiple criteria varying from payment history, credit utilization, affordability, and many more. The commonly used credit score FICO® designates 850 (100%) as the “perfect” score, and anything above 670 can be considered as “good.”

What Is a Great FICO® Score?

The FICO® scale might consider 670 to be a good score, but for many lenders, “good” simply isn’t good enough. You need to push this boundary and rank amongst the top 50% of Americans to enjoy the benefits of high credit-worthiness.

How long does it take to improve a credit score?

Apart from the rare miracles, the general fact is: there is no overnight solution to improving your credit score. Calculating credit scores is a complicated process, and even the fastest measures may take months to reflect.

- Start by checking your credit report for errors.

- Pay down your credit balances to lower your credit utilization ratio.

- Settle accounts that are in collections and make your delinquent accounts current.

If all else goes well, with these changes, you can see significant improvement in your credit score in 30-90 days.

How to check your credit score?

To check your credit score, you have to refer to places where it may have been used (not in your credit report). Like credit card debt, loans, and other debt. Check their monthly/quarterly/yearly statements. Major Credit Rating Agencies also allow you to purchase your credit score directly. Or there are plenty of online tools that can do it for a minimum fee or for free.

If it’s the credit report you want to check, the top three credit bureaus (Equifax, Experian, and TransUnion) now provide six free credit reports per year. Open a free account with them, log in, and request your report – that’s it!

What Affects Your Credit Score

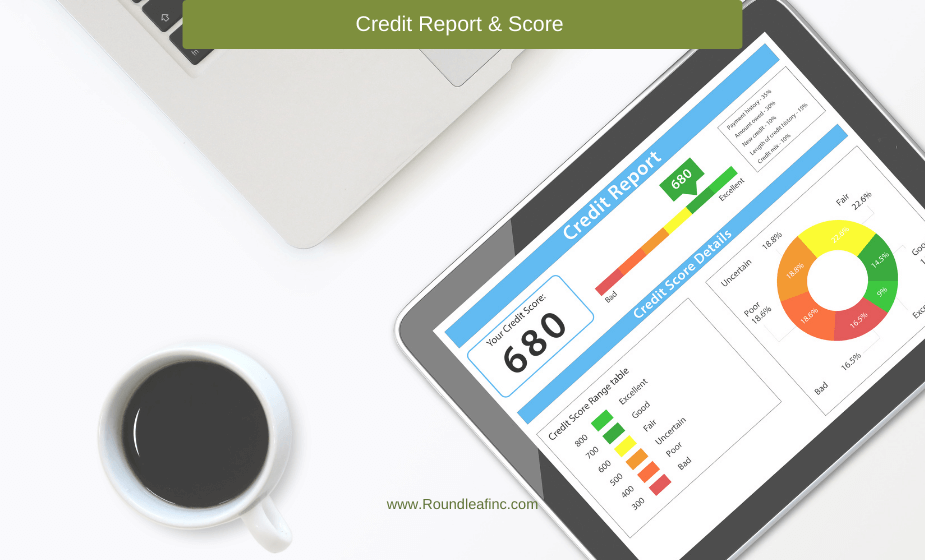

Payment history is the most weighted factor (35%) in determining your credit score. Even one late payment can hurt it badly. Other factors that affect it are credit utilization ratio (30%), the length of your credit history (15%), your current credit portfolio mix (10%), number of newly opened credit accounts (10%), and hard inquiries connected to them. Foreclosures, bankruptcy, repossession, charge-offs, and settled accounts can also negatively impact your credit score.

Credit Score Evaluation (with weightage):

- Credit Payment History (35%): Historical data on past debt repayments are scrutinized by rating agencies to analyze your sense of responsibility to pay debts on time.

- Debt-to-Credit Utilization (30%): The ratio percentage between the debt you accumulate vs. the total credit limit on credit accounts give a picture of your affordability. Ratios beyond 30% can work against you.

- Credit History Length (15%):Longer credit histories mean steady relationships with lenders. Also, this gives credit agencies a better sampling for your payments. Ideally, a minimum of six months is needed to establish credit and get a credit score.

- Credit Portfolio Mix (10%): A balanced and diversified portfolio shows prowess in financial knowledge. Having different types of credit accounts like store credit cards, personal loans, secured credit cards can boost your credit scores.

- New Credit Accounts (10%):Credit lines opened recently gives the current picture of your financial stability. It also confirms patterns from your credit history. More the accounts, the higher the debt-to-credit ratio. This can have a negative impact on your credit score. Also, hard inquiries and rejections show in your credit report.

Potential Lenders Looking into Your Credit

A typical lender looks primarily for two things when you ask for money:

- your capacity to pay back, and

- your intention to do so.

When you ask the same from an institution, it is not you but your credit report that presents your case.

The lending institution will look at your income or your ability to pay. They will judge your competence by your list of assets that you can use for collateral, your credit history that displays your commitment, and then compare your claim from your loan application to cross-check its feasibility.

What does your FICO® score mean to lenders?

- Exceptional (850-800):Lenders’ blue-chip candidate. You get first preference on the list of applicants, the best features, and rates on credit accounts.

- Very Good (799-740):Still great as a candidate, you receive better than average credit ratings from most lenders.

- Good (739-670):Only 8% of the applicants of your range are likely to become delinquent. Lenders are cautious but will rarely reject you based on the score alone.

- Fair (669-580):Considered as subprime borrowers, trust for these candidates vary from lender to lender. Credit applications are accepted after scrutiny.

- Very Poor (579-300):Bottom of the barrel candidates. Lenders generally demand security deposit to accept applicants from this score range. Lower-end of the range is virtually non-existent to them.

Credit History & Credit Score

How to build a good credit history?

The foundation for a good credit history lies with showing responsible behavior when it comes to finances. Good financial habits like borrowing only what you can afford, keeping your credits well within the specified limits, making on-time payments can go a long way.

Do not exploit your credit capacity by opening multiple accounts right at the beginning. Paying your balance in full is another way to impress your creditors. Be loyal to your accounts, and let them grow old. This showcases consistency and adds to your credit reputation.

How to improve credit score with no/bad credit history?

The trick to building your credit reputation from scratch is to start small. Do not jump to buying a house or leasing a car with zero credit.

- Become an authorized user of an existing credit account, like a family member’s credit card.

- Apply for a secured credit card, which has lesser scrutiny in terms of credit score. Typically, your credit lineis based on your deposit to your credit card.

- Build your credit score gradually by paying utility and cell phone bills from your credit line every month.

- Improve your credit score by availing the expertise of credit counseling agencies.

What Does & DOESN’T Improve Your Credit Score

Popular Notions that have Little to No Impact on Credit Scores

- Paying off early:

While this may seem like a good idea, but it doesn’t have much effect on your credit score. It does keep your hands clean from excess debts. That’s why this strategy mostly works with a debt consolidation loan in place. Otherwise, it’s better to keep installment loans open and make a timely monthly payment.

- Paying in full:

The zero balance scoring model is the one that crosses out paid in full collection debts. If your credit scoring agency is using the newer model (like FICO® 9 or VantageScore 3.0), then only it makes sense to pay off debts in full. In older models, like for bank mortgages, the paid collections will still show on your credit report.

- Paying off delinquent debts:

Paying off delinquent debts is a case of “too little, too late” as far as credit scores are concerned. But it does improve your credit history and makes a good impression towards lenders who give more importance to the actual credit report than just the score.

- Overdrafts:

Debit cards pull money from checking accounts. So even if you spend more than your account balance, you are not practically borrowing money from anyone. You may incur an overdraft fee, but it doesn’t impact your credit score in any way.

How long does negative info stay on your credit report?

CREDIT ACTIVITY |

SCORE IMPACT (NEGATIVE) |

RECOVERY TIME |

| Hard Inquiry | 2 years | |

| Delinquency (30+ Days Late) | 60-110 pts. | 7 years |

| Charge-Off | 45-125 pts. | 7 years |

| Student Loan Default | 7 years | |

| Foreclosure | 85-160 pts. | 7 years |

| Lawsuit / Judgement | 7 years | |

| Bankruptcy | 130-240 pts. | 7-10 years |

What makes your credit scores actually go up?

Paying on time:

Not paying on time is the most common mistake found on credit reports. No wonder, it would have the highest weightage on your credit score. Do not be late on payments. Every default stains your credit report, damages your credit history, and builds mistrust amongst lenders.

Having a secured credit card:

Secured Credit Cards are an excellent way to re-establish your credit. They require lesser scrutiny due to the security deposit being paid upfront. If you can maintain the card with regular transactions and timely payments, it gets added to your credit report and effectively improves your credit score.

Know the actual truths behind rebuilding your wealth and credit potential. Enroll in Roundleaf’s Credit Education Programs for a prosperous and secure financial future.